Disclaimer: The information in this blog post (“post”) is provided for general informational purposes only, and may not reflect the current law in your jurisdiction. No information contained in this post should be construed as legal advice from www.signalmagician.com or the individual author, nor is it intended to be a substitute for legal counsel on any subject matter. No reader of this post should act or refrain from acting on the basis of any information included in, or accessible through, this Post without seeking the appropriate legal or other professional advice on the particular facts and circumstances at issue from a lawyer licensed in the recipient’s state, country or other appropriate licensing jurisdiction.

Introduction

FOREX trading is becoming increasingly open and accessible to any who take an interest, both for aspiring full-time traders and a new breed of ‘social traders.’ Developing technology, combined with the wide scale proliferation of social and online networks has made it increasingly easy for investors to share and copy trading signals.

Two propositions that arose from this were Mirror Trading and, more recently, Copy Trading. The first is a simple evolution of automated trading which implements fixed strategies based on trading preferences. Investors copy all positions made by the experienced trader with account activity being automatically controlled by a service provider.

Copy Trading builds on this concept by allowing investors to set proportions between their account and that of the experienced trader as well as providing further risk management choices. The copying trader may also disconnect their funds and manage their own investments, closing the relationship.

Platforms have grown out of the concept of Copy Trading that allows everyday traders to send trade signals to potential clients. These clients may then choose to copy their strategies based on factors such as investment performance to date. The copied trader usually earns a monetary bonus based on the number of traders copying their position whilst the platform earns a subscription fee.

Whilst competing against other traders on existing Copy Trading platforms is one way to increase the earnings a trader can make an alternative is to develop their own Copy Trading platform or business. However, traders who choose to do this must be mindful of the regulatory environment in which they operate. Regulatory requirements have been established in countries across the world to ensure that client money is protected and these can impact on Copy Trading businesses. Requirements will differ based upon the country within which the business is established as well as its operating model.

The purpose of this paper is to provide a summary of the research and guidance issued by the various regulatory bodies on the subject of Copy Trading. It will highlight how regulation impacts Copy Trading businesses in the U.K. and the U.S. as well as how it applies to different operating models.

Copy Trading Business Model

Understanding the standard Copy Trading business model is important in highlighting what regulation will apply in each country. We will cover how altering this business model may change regulatory requirements (on a country by country basis) under exemptions sections later in this paper.

A basic Copy Trading business is made up of three main agents:

- The signal provider

- The client

- The service provider (platform)

The signal provider is usually an experienced trader who sends trade signals for others to copy. They require a platform with which to transmit these signals.

The client is the copier. They are the individual who chooses to mimic the trading strategies of the signal provider based upon the information available to them via the platform.

Finally, there is the service provider or the platform. The service provider allows the client to choose a signal provider (experienced trader) to copy as well as executing, or transmitting orders for execution, on their behalf.

The purpose of Signal Magician is to allow signal providers to also become service providers. In other words, it allows a trader to quickly operate a Copy Trading platform where clients can observe and copy their trades.

Copy Trading within the UK

Introduction to the UK Regulatory Environment

Traders looking to set up their own Copy Trading business should have a broad understanding of the UK regulatory environment and how it applies to their business.

Following the Financial Services Act 2012, three regulatory bodies were established in the UK. These were:

The Financial Policy Committee “FPC” which looks for future systemic risks to the overall financial system as well as providing high-level regulatory guidance

The Prudential Regulation Authority “PRA” which regulates firms seen as systemically important to the financial system i.e. ‘too big to fail.’

The Financial Conduct Authority “FCA” is the final body which is responsible for the prudential and conduct regulation of firms in the UK which provide financial products to the UK and international customers

As a smaller business and one which is not systemically important to the UK financial system, Copy Trading falls within the remit of the FCA.

The Financial Services and Markets Act 2000 (“FSMA”) states that any firm that carries out a regulated activity within the UK must be authorized or registered by the FCA unless they are exempt. Firms may be registered instead of authorized if they operate in a lower risk environment with registration being a stripped back form of authorisation1. However, this does not apply to Copy Trading.

What are regulated activities?

The regulated UK financial activities are fully explained in Part 2 of FSMA as well as the FCA website. The activities that are most closely associated with Copy Trading businesses are detailed below:

- Investments: dealing in or managing (as a principal or agent), arranging deals, safeguarding and administering, advising

- Options

- Futures

- Contracts for differences

Regulated activities are referenced to explicit investments within the FCA handbook (such as options, futures, and contracts for differences as above). For example, futures and contracts for differences in foreign exchange are highlighted within FCA regulation. It is not the underlying that is important, in this case, foreign exchange, but the investment itself i.e. an equity future would be treated as a designated investment by the FCA in the same way as a foreign exchange future.

Does European regulation also apply to Copy Trading?

European regulation does also apply to Copy Trading firms in the UK where that regulation has been transposed. Copy Trading businesses should be aware of the Markets in Financial Instruments Directive (“MiFID”). MiFID is the EU legislation that regulates firms who provide services to clients linked to ‘financial instruments’ (shares, bonds, units in collective investment schemes and derivatives), and the venues where those instruments are traded. MiFID has been adopted by European Economic Area states (and fully by the UK). Compliant firms can ‘passport’ their services to other member states. Being MiFID compliant, even if not required, is the only means to passporting in this way.

Firms that fall under the scope of MiFID need authorisation by the FCA as well as meeting further requirements as laid out under MiFID.

In summary, any Copy Trading business looking to operate in the UK should be aware of potential regulatory requirements as laid out by the FCA and under MiFID. and so should be taken into consideration.

Application of FCA and MiFID regulation to Copy Trading businesses

The high-level FCA stance on Copy Trading is as follows:

Copy trading allows investors to trade by automatically copying another investor’s trades, and we generally classify it as portfolio or investment management

Specifically, the FCA classes Copy Trading as portfolio or investment management where no manual input is required by the client. This agrees with the European Securities and Markets Authorities (“ESMA”) guidance on how Copy Trading applies under MiFID.

Under this definition, the view applied by the FCA and under MiFID is that Copy Trading businesses exercise investment discretion by automatically executing the trade signals of third parties, as agreed upon under a client mandate. In any situation where there is no manual intervention from the client, the Copy Trading business model will be viewed as portfolio management and FCA authorisation will be required. This applies in all situations i.e. neither the clients’ ability to set risk parameters nor the installation method for Copy Trading software would lead to exemptions from authorisation.

Exemptions from UK regulation for Copy Trading businesses

Those looking to start a Copy Trading business within the UK should be aware that in almost all scenarios and business models FCA authorisation is required. It is also recommended as authorization gives clients confidence in the business and assurance that their money is well looked after.

Based on the above, total exemptions are almost impossible to achieve for Copy Trading businesses. Owners should instead understand how the complexity of their business model can be reduced, which in turn reduces the regulatory requirements as laid out under MiFID and by the FCA.

Is it possible for a Copy Trading firm to gain exemption from MiFID?

In theory, it should be technically possible for a Copy Trading firm, offering a FOREX service, to be exempt from MiFID.

All ‘investment firms’ fall under the scope of MiFID and therefore require FCA authorisation. At present, there is the possibility for Copy Trading firms to fall outside of the definition of an ‘investment firm’ by only allowing trading in spot FX contracts (anything that leans toward a derivative contract will be covered by MiFID). However, this could be overly restrictive and ongoing updates to MiFID regulation may change this.

This also does not exempt Copy Trading firms from potential authorization requirements under the Financial Services and Markets Act i.e. investments as shown in section 3.

On balance, gaining exemption from MiFID will likely not be worthwhile for a Copy Trading business within the UK due ongoing regulatory updates as well as it is likely that the firm will still require some form of FCA authorisation.

Can changing the business model lead to any regulatory exemptions?

This deals with reducing regulatory requirements instead of avoiding them altogether. Both the FCA and MiFID class Copy Trading as portfolio management where client orders are automatically executed.

However, if the business model is changed so that manual client intervention is required ahead of each order, the activity no longer amounts to portfolio management.

In terms of a Copy Trading, this means that as long as clients are given the option to accept or reject a trade, the business activity will not be classed as portfolio management and so will not trigger regulatory requirements under MiFID and the FCA such as a suitability assessment.

Allowing manual intervention in this way simplifies the regulatory requirements of the Copy Trading business. Authorisation will now only be required for the activities of ‘reception and transmission of client orders’ and ‘investment advice.’

Is it possible for a Copy Trading firm to avoid providing ‘investment advice’?

No. Copy Trading firms will be deemed as providing investment advice, even if no explicit advice is given, as they are offering the possibility for a deal to occur. This applies to the traditional means of Copy Trading as detailed in section 2 i.e. trades are sent to client account for execution.

Could a Copy Trading firm become a licensed representative of another authorized firm and, as such, not require authorization?

There are some broad exemptions from MiFID that are relevant to insurers, group treasurers, many authorized professional firms, professional investors who invest only for themselves, pension schemes, depositaries and operators of collective investment schemes or other collective investment undertakings (such as investment trusts), journalists, and commodity.

More specifically, these exemptions apply when investment services are offered in an incidental manner in the course of a professional activity that is subject to legal or regulatory provisions or a code of ethics.

So what does this mean for a Copy Trading business? Theoretically, it means that where Copy Trading services are offered in an incidental manner to the activities of a professional firm, as detailed above, no authorization would be required.

However, whilst this may be possible, defining an incidental activity gives rise to its own complexities. To be incidental, any Copy Trading service would have to be required by the business but fall outside of the scope of its main offering. Further clarity on this concept is difficult and would likely be assessed on a case by case basis.

Would offering an EA rental option instead of traditional Copy Trading require FCA authorisation?

Offering an EA rental option essentially changes the Copy Trading business model. Instead of trades being copied from a master account clients simply rent an EA. From a regulatory standpoint, this would no longer be defined as Copy Trading and as such would not fall under standard Copy Trading regulation e.g. Portfolio Management or Investment Advice.

Current research into both FCA and MiFID regulations would not suggest that renting an EA would require any form of authorisation. Whilst the EA may relate to financial instruments that fall under MiFID there is no clear regulated activity taking place. Investment Advice is the most likely classification of this activity, however, the FCA handbook states that:

Merely providing information to clients should not itself normally amount to investment advice. Practical examples include:

- merely explaining the risks and benefits of a particular financial instrument;

- producing league tables showing the performance of financial instruments against published benchmarks.

Hence, renting an EA to a client based on a display of its performance, which the client can test using a demo account is unlikely to amount to investment advice or any other regulated activity requiring authorization.

Do countries outside of the UK or EEA require FCA authorisation to conduct Copy Trading activities within the UK?

Firms operating within the EEA, but outside of the UK, can apply for a ‘passport’ to operate within the UK itself. The type of passport required will vary based upon the service proposition, for example, a FOREX Copy Trading business will need a specific form of a passport. In most cases, the firm will also require authorisation by the local countries regulator (although authorization requirements can often be less stringent). An example of this would be the recent influx of FOREX firms established in Cyprus who have passported into the UK.

For non-EEA firms, for example, the UK branch of a US firm, European regulations such as MiFID do not apply. However, if MiFID would have applied to a firm had it been incorporated or formed in the EEA, it will be classified as a third country investment firm under the FCA’s rules. As a result, certain MiFID based requirements would then apply.

Finally, non-EEA firms who wish to undertake regulated activities within the UK should be authorized by the UK for that activity. Regulation is based on where the specific activity takes place i.e. if Copy Trading is offered within the UK then it falls under UK regulatory requirements (the exception being a passported company from within the EEA).

Summary of regulatory requirements for Copy Trading businesses within the UK

Copy Trading businesses who wish to operate within the UK should be aware of regulation required by the FCA and under MiFID. Authorization will be required by the FCA although firms can reduce the complexity of this authorization by adapting their operating model. Exemptions from MiFID are also possible although likely to be too restrictive.

Despite regulatory requirements, a Copy Trading business within the UK has the potential to be extremely viable. Regulatory requirements are in place to protect consumers but they also provide reassurance and credibility to those firms that adhere to them. In this way, a Copy Trading firm that acquires authorization (which is not a necessarily complex process) may lead to higher long run profitability. The success of other Copy Trading platforms in the UK, such an eToro, is a testament to this.

Copy Trading within the US

Introduction to US Regulatory environment

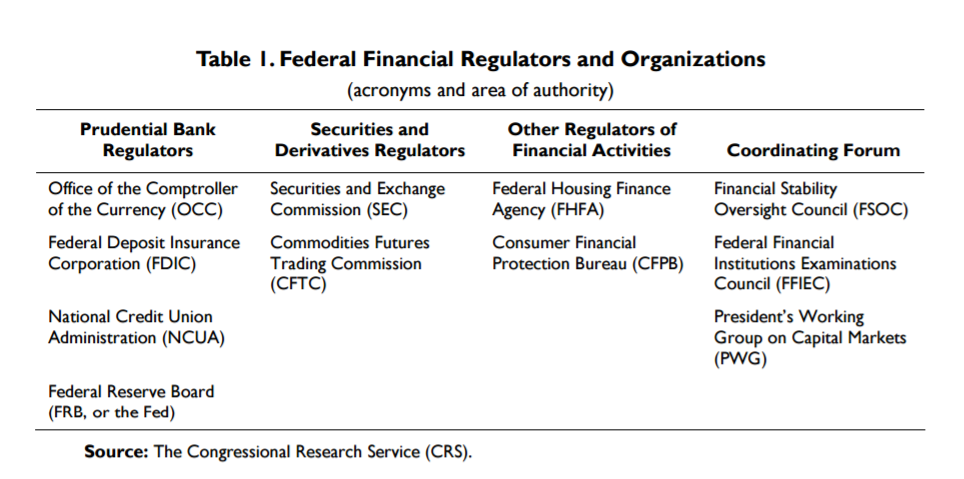

The US financial system is regulated through several channels (see table below) however, the majority of these regulators are not relevant to Copy Trading businesses. Two Securities and Derivatives Regulators; the ‘SEC’ and the ‘CFTC,’ are primarily relevant.

Securities and derivatives regulators monitor exchanges that host the trading of financial contracts, oversee the disclosures that market participants provide, and enforce rules against deceptive or manipulative trading practices.

Securities, Derivatives, and Similar Contract Markets Federal securities regulation has traditionally focused on disclosure and mitigating conflicts of interest, fraud, and attempted market manipulation. Securities regulation is designed to ensure that market participants have access to enough information to make informed decisions, rather than to limit the riskiness of the business models of publicly traded firms.

Firms that sell securities to the public must register with the Securities and Exchange Commission (SEC). SEC registration in no way implies that an investment is safe, only that material risks have been disclosed. The SEC also registers several classes of securities market participants and firms. Although the SEC is concerned with ensuring the safety and soundness of the firms it regulates, its primary concern is maintaining fair and orderly markets and protecting investors from fraud. Two types of firms come under the SEC’s jurisdiction: (1) all corporations that sell securities to the public and (2) securities broker/dealers and other securities markets intermediaries. Firms that sell securities—stocks and bonds—to the public are required to register with the SEC. Registration entails the publication of detailed information about the firm, its management, the intended uses for the funds raised through the sale of securities, and the risks to investors.

Derivatives trading is supervised by the Commodity Futures Trading Commission (CFTC), which oversees trading on the futures exchanges, which have self-regulatory responsibilities as well. The CFTC was created in 1974 to regulate commodities futures and options markets. The CFTC’s mission is to prevent excessive speculation, manipulation of commodity prices, and fraud. Like the SEC, the CFTC oversees industry self-regulatory organizations and requires the registration of a range of industry firms and personnel, including futures commission merchants (brokers), floor traders, commodity pool operators, and commodity trading advisers.

The CFTC is the regulator with which Copy Trading businesses should be concerned and any information provided below will be focused to this effect.

Regulation specific to Foreign Exchange trading

No agency is granted sole authority to regulate the mechanics of foreign exchange trading, except to the extent foreign exchange futures are offered on regulated exchanges. It is through the interaction of both the SEC and CFTC that trading of FOREX is regulated as it is for many other financial instruments.

Application of US Regulation to Copy Trading Businesses

The way that US regulation applies to Copy Trading firms, whether FOREX based or not, is again very much linked to the business model of the Copy Trading business.

Under the standard structure highlighted in section 2 (think of this in terms of common Copy Trading platforms such as eToro) the Copy Trading business would be classed as an ‘Introducing Broker.’ An introducing Broker is defined as:

An IB is an individual or organization which solicits or accepts orders to buy or sell futures contracts, options on futures, retail off-exchange forex contracts or swaps but does not accept money or other assets from customers to support such orders.

This definition applies to all forms of contract i.e. FOREX would fall within this definition.

Alternatively, if a Copy Trading business were deemed to be providing investment advice it would need to be registered as a Commodity Trading Advisor. A Commodity Trading Advisor is defined as:

A CTA is an individual or organization which, for compensation or profit, advises others as to the value of or the advisability of buying or selling futures contracts, options on futures, retail off-exchange forex contracts or swaps.

Providing advice includes exercising trading authority over a customer’s account as well as giving advice based upon knowledge of or tailored to customer’s particular commodity interest account, particular commodity interest trading activity, or other similar types of information

The importance here is the specificity of advice and the exercise of trading authority over a customer’s account. In other words, providing generic advice that isn’t tailored to specific clients wouldn’t lead a company to be defined as a CTA. Similarly, if no authority is exercised over the client account (and specific advice is not provided) e.g. executing orders for clients, then the company should not be classified as a CTA.

For example, a firm that sends SMS messages to a client based on their risk return preferences but excludes others (with different risk return requirements) then this would be specific advice which would require CTA registration. If this same firm sent generic advice, but automatically executed orders in the client account, then it would also be classed as a CTA. On the other hand, if generic SMS advice was provided and execution was left up to the discretion of the client, then CTA registration should not be necessary.

Both Introducing Brokers and Commodity Trading Advisors are required to register with the CFTC as well as becoming a member of the National Futures Association. However, as stated above, different Copy Trading structures lead to different regulatory requirements. These will be covered across the following section.

Application of US Regulation to Copy Trading Businesses

As with the UK, in the majority of cases Copy Trading businesses will require registration. Again, it is recommended to do so as this assuages the doubts of customers and ensures proof that the business operates in a credible manner.

That said and, as quoted on the CFTC website, not all ‘commodity trading systems’ require registration, where commodity trading systems are defined as the following (and include FOREX):

- Computer programs that signal when to buy and sell commodity futures and options contracts

- Signals are based on mathematical formulas and are typically technical analyses of trading data, such as trading volume and prices

- Signals are not based upon fundamental analyses of economic factors, such as supply and demand

- Technical analysis attempts to predict future price movements based on historical prices, price relationships and price trends

The above list simply shows the broad classification the CFTC gives to commodity trading systems – these systems will require registration unless they are exempt. The CFTC gives some guidance on these exemptions, specifically stating that ‘not all system promoters are required to be members of the National Futures Association or registered with the CFTC.’ Exemptions falling under this will be covered in the section that follows.

What exemptions are available for Copy Trading businesses?

The principal exemption relates to Copy Trading businesses that fall within the definition of Commodity Trading Advisors. A direct excerpt from the National Futures Association website states the following:

In March 2000, the CFTC adopted CFTC Rule 4.14(a)(9) to create an exemption from registration requirements for CTAs that provide standardized advice by means of media, such as newsletters, pre-recorded telephone hotlines, Internet Web sites, and non-customized computer software. Also, the CTA may not direct client accounts.

“Whether a third-party system developer is required to be registered as a CTA depends on the particular facts of each case,” says Hirst. “In some cases, the third-party system developer may be required to register as an Introducing Broker (IB) if it refers customers to an NFA Member and receives compensation for the referrals.

In line with the above, a Copy Trading business that just provides standardised advice i.e. not personalised to individual customers in any way, will be exempt from the registration requirements of CTAs (provided that no discretion is exercised over the client account such as automatically executing orders).

An example of this could be to simply provide access to the trading strategies of other, or individual, traders for clients to copy. This could be done through a subscription services that allows clients to observe the trades of others in real time or through a generic alert system such as email, phone call or text message. An individual could also allow others to view their own trades by adopting the same model to the above.

More specific NFA guidance states that the following would be exempt from the need for NFA registration:

- You make recommendations, such as advice to buy or sell specific futures contracts should a particular price level be reached, through newsletters, books and periodicals. The advice includes specific recommendations and the recipients of publications all receive the same advice or

- You conduct seminars at which you teach attendees how to trade commodity futures contracts aided by a software program that you sell and you invite seminar attendees to participate in a question-and-answer session at which you provide commodity trading advice without asking or receiving information about the personal characteristics of the attendees

Any Copy Trading business operating under the above exemptions should be mindful of its Introducing Broker requirements if it falls in line with the conditions set out above.

Lastly, a Copy Trading business using this exemption may wish to add further detail to its terms and conditions as an additional layer of protection. See below for an example extract:

8.2. XYZ Ltd IS NOT A REGISTERED INVESTMENT ADVISOR, BROKER/DEALER, FINANCIAL ANALYST, FINANCIAL BANK, SECURITIES BROKER OR FINANCIAL PLANNER. XYZ IS A TECHNOLOGY PROVIDER WHICH AMONG OTHER THINGS FACILITATES THE SHARING OF TRADE INFORMATION VIA THE INTERNET. USERS OF THE SERVICE MAY USE THE TRADE INFORMATION TO FORMULATE THEIR OWN INVESTMENT DECISIONS WHICH COULD BE TO COPY THE TRADES OF OTHERS. ALL INFORMATION ON THE XYZ.COM IS PROVIDED FOR INFORMATION PURPOSES ONLY. THE INFORMATION IS NOT INTENDED TO BE AND DOES NOT CONSTITUTE FINANCIAL ADVICE OR ANY OTHER ADVICE, IS GENERAL IN NATURE AND NOT SPECIFIC TO YOU. BEFORE USING THE COMPANY’S INFORMATION TO MAKE AN INVESTMENT DECISION, YOU SHOULD SEEK THE ADVICE OF A QUALIFIED AND REGISTERED SECURITIES PROFESSIONAL AND UNDERTAKE YOUR OWN DUE DILIGENCE. NONE OF THE INFORMATION ON OUR SITE IS INTENDED AS INVESTMENT ADVICE, AS AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL, OR AS A RECOMMENDATION, ENDORSEMENT, OR SPONSORSHIP OF ANY SECURITY, COMPANY, OR FUND. THE COMPANY IS NOT RESPONSIBLE FOR ANY INVESTMENT DECISION MADE BY YOU. YOU ARE RESPONSIBLE FOR YOUR OWN INVESTMENT RESEARCH AND INVESTMENT DECISIONS.

Would offering an EA rental option instead of traditional Copy Trading require registration?

Regulation on this point, as in the UK, is less clear but would likely tie in with the standardized advice offering above. If all clients simply rented access as a form of ‘non-customised computer software’ then registration would not be necessary. However, Copy Trading businesses should again be aware of the regulation relating to Introducing Brokers as per the definition of an Introducing Broker provided in the previous section. Again, more specific NFA wording on what would be classified as an exemption is provided below:

- You provide advice through e-mails, facsimiles, an Internet web site, telephone calls or face-to-face meetings with customers consisting of instructions to buy or sell a futures contract based on a computerized trading system, which also is available for purchase and use on a personal computer, and the customers all receive the same advice

In this case the computerized trading system would be the EA and should not require registration as all clients get ‘generic advice’ from its use.

Do countries outside of the US require registration for Copy Trading activities within the US?

The CFTC states that ‘those persons located outside the U.S., who are subject to a comparable regulatory framework in the country in which they are located, may seek an exemption from registration.’ Commodity Trading Advisors without a US office also fall under this definition (seemingly without requirement for foreign regulation).

For example, a UK based firm that is regulated by the FCA could submit for exemption in the US as it would be deemed to be regulated to similar levels. A list of organisations, their home countries and the status of their exemption can be accessed through this link and will provide a deeper understanding of the likelihood of receiving an exemption.

In order to operate without registration within the US these firms must submit an exemption form that can be located on the CFTC website. The process involves a degree of scrutiny by the NFA to assess validity.

Summary of regulatory requirements for Copy Trading businesses within the US

As with the UK, Copy Trading businesses (whether relating to FOREX or not) are recommended to seek registration. Registration is a means of providing assurance to customers but, more importantly, ensures that the business can operate in the way it seeks to. However, exemptions do exist and are primarily related to the provision of standardised advice through standardised channels. There is no one recommended way of doing this so firms can be creative in the services they choose to offer.

Sources

https://www.fca.org.uk/firms/copy-trading

https://www.esma.europa.eu/sites/default/files/library/2015/11/2012-382.pdf

http://www.hsbcnet.com/gbm/attachments/bestexecution/mifid-annex1-sectionc-financial-instruments.pdf

https://www.fca.org.uk/publication/documents/mifid-ii-application-notification-guide.pdf

https://www.handbook.fca.org.uk/handbook/PERG/13.pdf

https://www.handbook.fca.org.uk/handbook/glossary/G1964.html

https://www.handbook.fca.org.uk/handbook/PERG/13/5.html?date=2016-06-17

https://www.fca.org.uk/firms/authorisation

https://www.fca.org.uk/firms/authorisation/regulated-activities

https://www.handbook.fca.org.uk/handbook/PERG/2/Annex1.html

https://www.handbook.fca.org.uk/handbook/PERG.pdf

https://www.nfa.futures.org/news/newsLetterArticle.asp?ArticleID=1380

http://www.cftc.gov/ConsumerProtection/FraudAwarenessPrevention/ForeignCurrencyTrading/index.htm

https://www.nfa.futures.org/nfa-registration/index.HTML

https://www.nfa.futures.org/news/newsLetterArticle.asp?ArticleID=1380

https://www.nfa.futures.org/nfa-registration/NFA-membership-and-dues.HTML

https://sirt.cftc.gov/sirt/sirt.aspx?Topic=ForeignPart30Exemptions

Darwinex, eToro,[3] FX Copy, ZuluTrade, Ditto Trade, Tradeo, Bretton Prime